Each such byte focuses on a functional issue startups need to solve as they build their company, from idea to scale. In this edition, we speak about the Indian accounting standards.

In the past couple of decades, we have witnessed innovative business models and growing outreach of Indian companies in the global arena. If your company has tried to access capital from any foreign investors, you might have also been asked to present your financial statements in line with global standards.

To facilitate capital raising and increase in foreign investments for domestic companies our government in February 2015 issued the Companies (Indian Accounting Standards [Ind AS]) Rules. Ind AS are in convergence with International Financial Reporting Standards (IFRS). Ind AS will enable your investors to compare investments across countries, as financial statements are prepared using the same set of global standards. If your company has a foreign subsidiary, adopting Ind AS can help by reducing regulatory compliance and costs. Implementation of Ind AS is expected to reduce the cost of capital since capital would be more accessible and easily available.

In our view, Indian regulators have done a laudable job by taking a giant leap to converge with IFRS. However, due to minor carve-outs and deviations between the two standards, Indian companies will not be able to state dual compliance with IFRS.

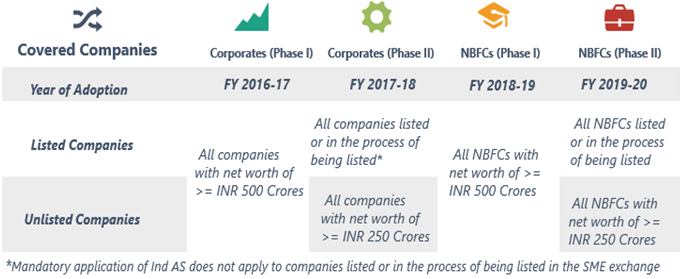

As per the notification, MCA necessitated Ind AS to be implemented in a phase-wise manner based on their net worth and listing status.

So, if your company is a listed entity or an unlisted company with a net worth of more than INR 250 crores you would have already adopted Ind AS.

It is important to note that Ind AS is not just a change in the way companies present their financial numbers; its implementation can have a significant impact on the reported earnings and net worth of your company. Some of these critical differences with Indian GAAP have been highlighted below: –

Ind AS 115, Revenue from contracts with customers, introduces a new single five-step revenue recognition model to ascertain the timing and amount of revenue to be recognized.

Performance Obligation – The Finance team of your company needs to ascertain if there are multiple promises in a contract and whether those promises are distinct. Moreover, if a transaction contains separately identifiable components (such as a bundled software contract along with necessary hardware components) Ind AS requires us to allocate revenues based on the fair value of each component.

Goodwill generated as part of a business combination has typically been amortized over a period under Indian GAAP as it is considered to have a definite life. Ind AS considers such goodwill to have indefinite life (mark the usage of the word ‘indefinite’, which is different from ‘infinite’), and hence no amortization is needed. Goodwill is tested annually for impairment. An impairment loss must be recognized if the carrying amount exceeds the amount to be recovered through the use or sale of goodwill. Similarly, all intangible assets with indefinite useful life will be tested annually for impairment loss if any.

Ind AS 116 on leases has removed the concept of operating lease. Now a single lease accounting model like financial leases is permitted for most categories of leases, under which they will have to be recognized on the balance sheet as a right-of-use asset. Operating lease allowed companies to just record rental expenses for leased assets without including the leased assets in their balance sheet. A financial lease, on the other hand, inflates the balance sheet by including right-of-use asset and a corresponding lease liability on the companies’ balance sheet. Depreciation of right-of-use asset and interest expense on lease liability is recorded annually in the profit and loss account instead of cash rental expense under an operating lease. Some implications:

Under Indian GAAP control is assessed based on majority voting rights and composition of the board of directors. Ind AS introduces a new definition of controlling rights under which investor (someone like Caspian) controls an investee (your company) if it satisfies all the following conditions: –

This implies that an entity which might have 0% equity stake, but has controlling rights owing to contractual obligations such as a lender relationship with rights of board membership (not triggered by an event of default), or can influence company as well as its returns (E.g.-Convertible debt holders of a company with additional controlling rights), might see a subsidiary relationship getting established!

Ind AS 32 Financial Instruments: Presentation requires financial instruments to be classified based on the substance of the contractual agreement rather than its legal form. Some of the key accounting differences because of this are that redeemable preference shares now get classified as a liability and the ‘dividend’ on such instruments are now recognized as interest expense (with obvious implications on reported profit). Another aspect of change is that compulsory convertible debenture would now be split into their liability and equity components while reporting, with the fair value of the estimated interest pay-out becoming the liability component. Combine this with the effect of changes caused by the revenue recognition policy under Ind AS, and anyone can guess the leverage your entity would reportedly be riding on!

The financial services industry has been significantly impacted by the implementation of Ind AS, more so around points like:

In conclusion, Ind AS gives a lot of emphasis on clear disclosures to investors and other stakeholders. Keeping the spirit of these principles intact while reporting under Ind AS (as opposed to adhering to guidelines in the erstwhile GAAP) will aid your company in its pursuit of growth funds too, as it complements the transparency metric key to many funders’ decisions. However, it is imperative for the companies to work closely with their auditors – at all stages – to ensure a comprehensive

https://m.rbi.org.in/scripts/BS_CircularIndexDisplay.aspx?Id=11818

conveying of business realities and computation methods in the disclosures. Ind AS requires segment reporting to be in line with the ones used by the management to make decisions, and the disclosure of judgments and assumptions used by the management. Disclosures of various risks impacting the company and corresponding sensitivity analyses also need to be provided for in the notes to financial statements. While the engagement with the auditors is going to increase (causing higher monetary & time costs), Ind AS inherently gives greater flexibility for the management to customize their accounts based on their unique business models & assumptions of growth – thus, driving more realistic financial reporting, a key need for entrepreneurs.

Please refer to these guidance documents by top accounting and advisory organizations to seek clarity on the various facets of Ind AS.

https://www.pwc.in/assets/pdfs/publications/2016/ind-as-pocket-guide-2016.pdf

https://www2.deloitte.com/content/dam/Deloitte/in/Documents/audit/in-audit-the-path-to-indas-conversion.pdf

http://gtw3.grantthornton.in/assets/Ind-AS/IND_AS.pdf

Let us know if you have questions or feedback. Reach out to us on info@caspian.in.