Decoding the terms and jargons in a debt term sheet for enterprises

At Caspian Debt, we interact with many first-generation entrepreneurs, and believe that it is our responsibility to make things simpler for them, as much as possible. The fast-growing enterprises today have options of raising debt funding from different type of institutions (Bank, NBFC, Debt funds) and knowledge of below-mentioned terms can be useful while navigating the documents and conversations:

- Credit Facility/Loan /Principal/Investment Amount: This is the amount of funds that has been sanctioned to the enterprise by the lender. The terms used here might vary due the type of the lender and nature of the product(loan/bond/debenture). Irrespective of the names, these refer to total amount of borrowing which has been sanctioned and is required to be repaid by enterprise.

- Tranche: The above-mentioned amount may be disbursed in parts, one or many as per the mutual agreement of lender and borrower. Each part is called a tranche.

- Coupon/Interest rate: This is generally the major income for any lender and major cost of borrowing for the borrower. It is paid periodically, mostly monthly, sometimes quarterly. It can be Flat interest rate or diminishing balance rate. A flat interest rate is applicable on the full amount of the loan throughout its tenure without taking into account the reducing principal amount as the loan is repaid. The diminishing balance interest rate is applicable on the outstanding principal, and the interest payments reduce with time. A flat interest will always appear cheaper than its actual cost to borrower, and should be treated as a red-flag if observed in term sheet.

- Processing fee/Charges: A fee, generally charged in terms of percentage on the sanctioned amount of credit facility/loan. Eg:2% on INR 1crore of loan becomes INR 2 lakhs. This is payable upfront at the time of funds’ disbursement. Some lenders deduct the fees from the loan amount before disbursing while some receive the fees before disbursement. Processing charges can also be charged before every tranche disbursement.

- Default Interest/Penal Interest: Any delay in repayment comes with a penalty. It is usually 2 to 5% per annum, either on the outstanding Principal or the amount overdue.

The Interest rate and processing fee are the primary income sources for a lender. However, there can be other ways too, via warrants/options/right to invest in equity at a discount. It is especially evident in a venture debt transaction. Watch out for such additional clauses.

- Tenor/Tenure: The duration in which the entire loan along with interest shall be repaid.

- Repayment schedule: A date-wise schedule for the interest and principal repayment by the borrower is known as repayment schedule. This can be flexible in some loan products like Cash-Credit and Overdraft. Any delay in the repayment results in a monetary penalty and bad credit history for the borrower. Hence, this needs to be carefully structured.

- Moratorium: The period where borrower can get a repayment holiday. It is generally applicable to principal repayment. It can be useful in situations where the borrowing enterprise might face a gap between incurring expenses for implementation and cash inflow from its customer, for example, a capital expenditure like setting up a hospital, manufacturing facility or purchasing an equipment. Traditional Banks/NBFCs offer very little flexibility in structuring repayments whereas specialised lenders like Caspian Debt try to schedule repayments to match the borrowers’ budgeted cashflows, and provide moratorium for some months if needed, and take seasonality of business into account.

- Collateral and Security:The lender may ask for security from the enterprise against the loan provided. The security can be primary or secondary. The primary security for an enterprise is the owned assets, and Secondary security is assets of a third party (usually the founders/promoters). Collateral is actually an alternative word for secondary security but the terms Collateral and Security are generally used interchangeably.

Specialised lenders like Caspian Debt rely more on business model, cashflows and lesser on security. In fact, they rarely ask for mortgage.

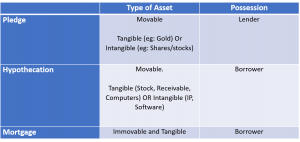

The most common forms of accepting a security are: Pledge, hypothecation, or mortgage. The difference is in terms of the type of asset and possession.

This right over security is established legally by the lender via a charge filed with Ministry of corporate affairs. The charge can be in the form of priority (first, second, third and so on) if there are multiple lenders, or pari passu, which means equal right over assets for multiple lenders.

- Guarantee: If a lender does not have the desired comfort on standalone borrower entity, it may ask for Personal guarantee (usually provided by the Promoters) or Corporate guarantee (an enterprise providing the guarantee, generally the parent company or investor).

There can be multiple variations within the above-mentioned clauses, but the broader purpose/terms remain similar. A prior understanding of the terms can help one negotiate smartly, avoid misunderstandings & unnecessary delays, and create a win-win scenario.

Hopefully, next time you see a debt term sheet from Caspian debt or anyone else, you will be better equipped to navigate the discussion.